This article is brought to you by Infinity Financial Solutions.

THE QUESTION OF how much you need to retire is such a tricky one to answer and a vast number of factors need to be taken into consideration. So much so, that many people just don’t bother and bury their heads in the sand, neglecting to think about the financial logistics of their retirement.

It’s often only until later on in life when panic sets in that people seek advice on the matter. They’ll have that lightbulb moment of realisation that they won’t always be fit, healthy, and able to work as they witness their own parents retiring and facing the challenges of ageing. It’s a wake-up call that they really do need to make provision for when they themselves stop working.

Obviously it’s better late than never although nothing beats steady, regular saving started as soon as you make your first steps on the career ladder. Clarifying your retirement needs in terms of income, savings required, and how you plan to achieve them is a crucial question and ideally one to be considered as early as possible in your career.

Figures released last year by the Office of National Statistics (ONS) in the UK reveal that the average retired household spends £21,770 per year. To get to that figure when you start saving in your 40s is, quite frankly, hard work. An individual who has made the requisite amount of contributions will be eligible for a state pension which is a not-so-generous £159.55 per week or £8,296.60 per year. That leaves a £13,473.40 shortfall from the average expenditure target to be made up by an individual. For expatriates having worked overseas for many years and have not paid voluntary class 3 NI contributions will have an even higher personal target.

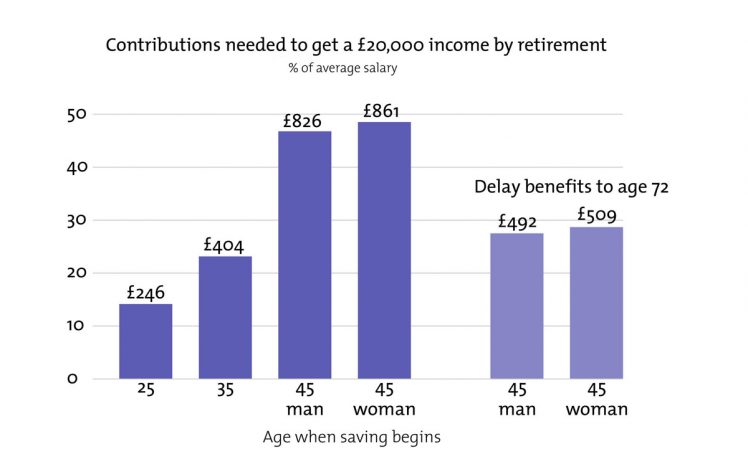

The table below shows just how much needs to be paid into a pension each month to obtain a £20,000 per year pension (in today’s monetary terms) from age 67.

You can clearly see just how much more difficult it becomes to attain even a modest retirement target for our 40 somethings who leave it late to start saving. They will need to put away almost half of their income in order to hit target, compared to 14% for the canny 25-year-old who gets ahead of the game. Seeing these figures, it is hard to underplay the cost of putting off saving for retirement.

The columns on the right show that delaying the age at which you retire will reduce pressure for our 40-something late savers but there is no guarantee you will be healthy enough to continue working into your 70s, even if you wanted to.

It’s also worth noting that these figures are for a rather modest pension and not likely to give anyone the financially worry-free golden retirement we all dream about. Especially for the average expatriate who have enjoyed much higher earnings and so therefore need a substantially higher pension pot to maintain such a standard of living.

Whichever way you look at it, it is clear that the vast majority of us need to save more than we are

currently doing. The desire for instant gratification in the modern world means that few people have any kind of long term financial vision but you can and should set yourself apart. If you feel that you can’t do it alone, you should seek assistance from a qualified Financial Adviser like myself. Our job is to assist you in quantifying your financial aims and devising, developing, and monitoring a plan to help you achieve them.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

Sam is a UK-qualified Independent Financial Adviser and strives to raise the standards of international financial planning in Malaysia. He has been based in KL since 2009 and represents Infinity Solutions Ltd in partnership with UK-based Wealth Manager – Tilney Group. You may direct any inquiries to sbarrie@infinitysolutions.com or call +6017.3499 686

This article was originally published in The Expat magazine (February 2018) which is available online or in print via a free subscription.